When owners move out of an HOA, they will have some added responsibilities before they can say a final goodbye to the neighbourhood. Different communities have different moving requirements; some may ask owners to complete a home inspection, transfer documents, or hand over other paperwork before transferring ownership.

If an owner owes money to the HOA, these fees need to be paid up before the home is sold. An estoppel letter can clear up any confusion about outstanding fees, and help ensure the HOA receives the money it is owed.

Common estoppel letter questions

- What is an estoppel letter?

- What is the purpose of an estoppel letter?

- What is included in the letter?

- How does someone obtain an estoppel letter?

- How much does an estoppel letter cost?

- What if the seller doesn’t owe the HOA any money?

What is an estoppel letter?

An estoppel letter is a legally binding document used to certify the amount of money that an owner who is selling their home owes to the association. Any outstanding fees that have not been addressed by the date specified in the letter, will appear on the document.

Different places use different names to refer to an HOA estoppel letter, including an estoppel certificate, HOA letter, HOA status certificate, HOA closing statement, and current dues letter.

Outstanding balances include all of the fees that the seller is delinquent in paying, such as:

- Current HOA fees

- Delinquent fees

- Interest payments

- Special assessments

- Attorney fees

An estoppel letter is legally binding, and once it has been submitted, the HOA cannot add newly discovered debts to the estoppel letter.

What is the purpose of an estoppel letter?

Estoppel letters protect new buyers from undisclosed financial obligations to the HOA left by the previous owner. Financial obligations are often included in negotiations to determine closing costs for the sale of a home. The new buyer is not responsible for paying any fees belonging to the current owner (even if the estoppel is incorrect). But, if the buyer does not receive an estoppel letter and closes on the property, then they could be responsible for all fees that the former owner didn’t pay.

The buyer also receives a warranty deed from the seller, which guarantees that the seller holds a clear title to the property, and that they have the right to sell it. The guarantee is backed up by a title insurance policy, which is purchased as a closing expense and provided to the buyer and their lender. Before a title company issues a policy, they will ensure that there are no liens on the property, and that all HOA dues are paid in full.

This document is equally important for lenders as it allows them to verify that the property for which they are lending the funds meets their lending regulations. Since the document shows fees charged against the current owner, the lender can see if the seller ever made unauthorized changes or upgrades to the property that were not corrected.

Finally, estoppel letters give HOAs an opportunity to request delinquent fees from busy owners who are probably more concerned about other moving tasks. Associations must ensure that they have included all fees in the letter; otherwise, years of delinquent fees could be lost.

What’s included in the letter?

There is no standardized template for estoppel letters; HOAs are allowed to create their own estoppel letters or forms, but are obliged to follow any processes and procedure laid out in the association’s bylaws, if they exist. They may also create their own request forms or processes, depending on what their bylaws say. Since there is usually a tight deadline for estoppel letter submissions, it may help to use an online system that streamlines these sorts of requests so that they are not forgotten.

Generally, estoppel letters will list the following information:

- Date of issuance

- HOA’s name and contact information

- Owner’s name and contact information

- Address and property description

- An itemized list of fees owed to the association

- The date for which the balance will remain unchanged, or if requested, what is owed through the date of closing

- Detailed payment instructions

- Authorized signature from a board member

How does a buyer obtain an estoppel letter?

It is usually the title company handling the closing that will request an estoppel letter from the HOA. The HOA is obligated to provide the estoppel letter, and an authorized representative from the association must complete and sign the document within a certain amount of time. Florida Statute states that the HOA must deliver the estoppel letter to the requested party within 10 business days after receiving a written or electronic request (it used to be 15 days, but the laws have changed).

Every Florida association is also required to designate a person or entity with a street or email address for receipt of a request for an estoppel letter, and share this information publicly on their website. The letter must be provided by hand delivery, regular mail, or email to the requestor on the date of issuance.

If the information is not delivered within 10 business days, the HOA cannot charge a fee for the preparation and delivery of the estoppel letter. Furthermore, A summary proceeding may be brought by the requestor to compel compliance, and the prevailing party is entitled to recover reasonable attorney fees.

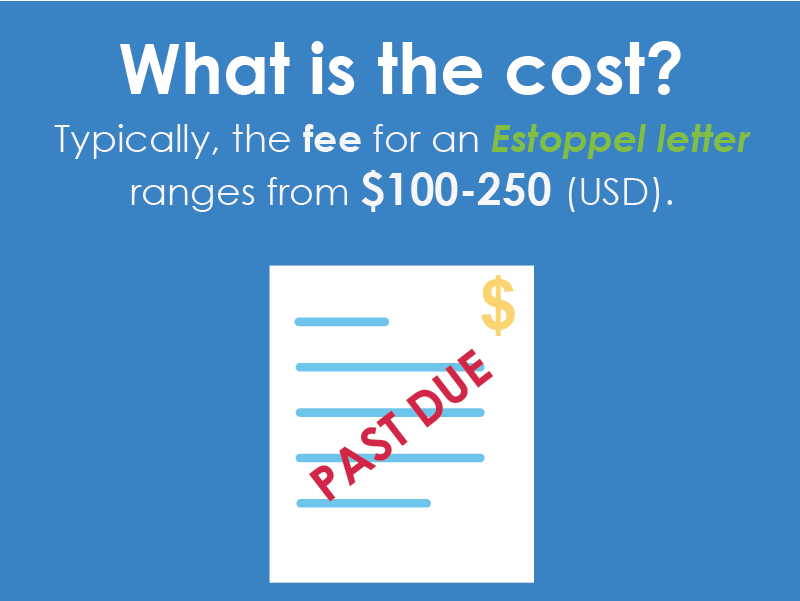

How much does an estoppel letter cost?

The HOA may charge a fee for preparing and delivering an estoppel letter. HOAs generally charge between $100 – $250 for the document. Florida law states that an association cannot charge more than $250 unless:

- the estoppel certificate is requested on an expedited basis and delivered within 3 business days after the request. In this case, the association may charge an additional fee of $100, or

- a delinquent amount is owed to the association. An additional fee of $150 for the estoppel letter may be charged.

So, there is a $500 limit for total fees that can be charged for estoppel letter preparation.

The person who pays for the preparation of this document (the current owner) may request a refund if the letter is requested in conjunction with the sale or mortgage of a home, but the closing does not occur. The request must be in writing, and must be received no later than 30 days after the anticipated closing date. Refunds must be issued within 30 days after the written request has been received.

What if the seller doesn’t owe the HOA any fees?

Even if a seller has an outstanding balance of $0, the estoppel letter must be given to the party that requests it, and the fee must be paid.

Conclusion

Before a new neighbour moves into an HOA, one of the many things they will need to do is obtain an estoppel letter from the association. The purpose of this document is to inform the buyer of any delinquent fees on a property before closing. A new buyer is always looking for a fresh start, and having to pay someone else’s fees would be a terrible beginning to a new chapter in their lives.

In order to avoid collection issues with owners who are preparing to leave the community, regular rule enforcement is key. By addressing issues regarding delinquent payments right away and working with owners when unexpected issues arise, members won’t have significant outstanding fees when it comes time to leave the community.

HOAs must take care to comply with all state laws and association bylaws governing estoppel letters. Time is precious in these situations, and deadlines should be taken seriously.